Click chart for enlargement

Photo: Gerry Boland Studio &

Department of Fisheries and

Aquaculture.

Fishing vessels at Polar Seafoods’

wharf, Corner Brook.

(Click on photo to visit Gerry

Boland Studio)

- Volume of landings expected to be on par with 1999 level of 258,000 tonnes.

- Markets to remain strong for most species.

- Expected permanent legislation will establish a price setting mechanism between harvesters and processors.

Aquaculture Production

1997 to 1999Production (Tonnes)

Species

1997

1998

1999

Salmonids

980

1,730

2,480

Mussels

750

950

1,700

Cod

30

10

100

Other

20

10

10

Total

1,780

2,690

4,290

Note: All numbers rounded.

Department of Fisheries and Aquaculture

FISHERIES

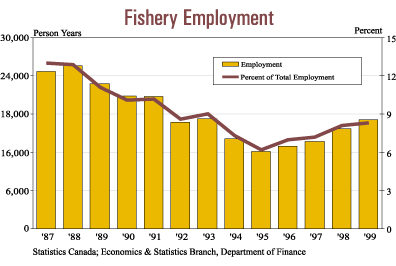

Landings rose by 4% in 1999 and record landed value ($518 million) and production value ($1 billion) were achieved. Employment was up 9% and new investment exceeded $125 million in the past two years.

The fishing industry has undergone significant structural change in the last decade following the closure of the Northern cod and other groundfish fisheries which once dominated the industry. Today’s fishery is increasingly efficient, market-driven, capital-intensive and professional. It is focused on development of new resource opportunities, secondary seafood production and aquaculture. Over 45 species are currently harvested and development, processing and marketing activities for other species are ongoing. There are over 100 commercial or developing aquaculture operations in the Province, generating $18 million in export value in 1999.

Many industry indicators were positive in 1999. Total landings increased for the fifth consecutive year, rising by 4% to 258,000 tonnes. Landed value rose 36% to a level almost double that recorded in 1996. Production value rose by 37%, reaching a record $1 billion. Average monthly employment in the harvesting and processing sectors increased to over 17,000, the highest level since 1993. Processing employment was particularly strong, increasing by 38% in 1999 to double its 1995 level.

Revitalization and growth of the fishing industry has been aided by various shellfish species including crab and shrimp, both of which were strong contributors to industry growth in 1999. Growth in the crab fishery was particularly strong in 1999 with landings rising by 31.4%. This growth saw crab landings reach a record 69,000 tonnes. It is possible that the snow crab biomass may have peaked and that some downward adjustment in landings may occur in the short term. Nevertheless, crab is expected to remain the dominant species over the foreseeable future.

Shrimp has also seen sizeable growth over the past two years. In 1999, combined inshore and offshore shrimp landings rose by 15.6% compared to 1998, and they were up almost 50% from 1997 levels. Further growth is expected in 2000 on the basis of increased quotas and effort. The shrimp fishery’s contribution to the fishing industry has been enhanced by the development of the inshore northern shrimp fishery which has resulted in increased capital investment in value-added processing capacity. Cooked and peeled shrimp plants now operate at ten locations.

Market prices for shellfish were mixed in 1999. Resource problems in Alaska, coupled with growing consumer demand, led to increased crab prices. Conversely, higher shrimp landings led to increased supply and a downward trend in market prices. Industry has mounted an aggressive promotional program for cold water shrimp and this initiative should impact positively on the industry.

Fisheries Policy Initiatives

Fisheries revitalization has been enhanced by policy initiatives related

to price negotiations, processing capacity, quality measures, and education

and training. In 1998, a two-year innovative model (Final Offer Selection)

for price settlement between fish harvesters and processors was introduced.

This model facilitated a timely start to six key fisheries in each of the

past two years and has been well received by industry stakeholders. The

pilot model has been extended into 2000 and legislation is being drafted to

allow for its continuation beyond this year.

A new processing policy was developed in 1997 to help increase the competitive position of processors by rationalizing capacity and lengthening plant operating periods while maintaining a regional approach to capacity. This policy established the core plant designation and provided for a quality assurance program as well as licence consolidation, transfers, and cancellation. The number of active fish plants has been reduced from 240 to 145 since 1997. Among active plants, 63 have attained core status.

The establishment of a Fish Harvesters Certification Board in 1997 placed a new emphasis on industry professionalization. In 1999, approximately 15,400 certified fish harvesters were registered with the Board. This included almost 8,900 Level II fishers, 1,300 Level I fishers, and almost 5,200 apprentices and new entrants. Any new fish harvester must meet specific education requirements and must have a minimum level of sea time. As well, the Marine Institute of Memorial University offers over 100 institutional and community-based courses related to harvesting, processing, food preparation and quality enhancement.